Repeal Indiana's Transit-Tax Statute

IndyGo Had No Intention of Complying with Its Fare-Recovery Requirement

Introduction

The Indianapolis City-County Council is not supposed to impose a transit income tax on Indianapolis residents unless the Indianapolis Public Transportation Corporation (“IndyGo”) has so set its fare prices that at least 25% of its fixed-route system’s operating expenses are covered by fare revenue. But the relevant statute’s drafting seems to have been based on the assumption that the Council could be relied upon to follow the law, whereas events have proved that it can’t. For six years IndyGo has received proceeds of a 0.25% income tax on residents without collecting the required 25% of its operating expenses from riders. Indianapolis residents have consequently paid over $300 million more in taxes than they should have.

This post will argue that at least by the time the tax was imposed IndyGo had no intention of complying with the 25% requirement and that the statute’s grant of power to impose the tax should therefore be repealed. Or, if it isn’t repealed outright, the statute’s fare-collection provisions should be made harder to evade, perhaps in one of the ways that our next post will propose.

Background

Like most American city-bus companies the one that has come to be known as IndyGo has long been too big for the city it serves. Nearly half a century ago it began resorting to government subsidies instead of right-sizing its operations as erstwhile bus riders became increasingly able to afford cars.

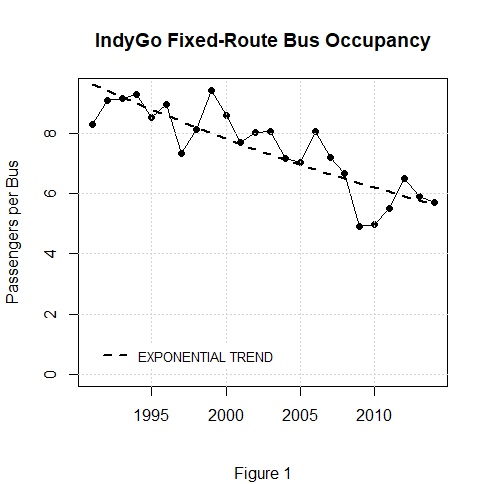

Its ridership trend since then has been generally downward, but a temporary surge occurred early in the last decade, when Indianapolis hosted the Super Bowl just as the nation emerged from the financial crisis and IndyGo began to fund added service with a special property-tax levy. During that period IndyGo together with other taxpayer-funded special-interest groups intensively lobbied the Indiana General Assembly for still more subsidy money.

This should have been a hard sell; almost no residents regularly ride the bus, and the modest ridership increase that was being seen at the time was probably (and has indeed turned out to be) just a temporary pause in the downward trend. As the plot above shows, moreover, there was evidence that IndyGo’s previous trend to emptier buses had resumed. So in considering a transit-tax bill a legislator might reasonably have asked himself whether further expansion wouldn’t just make the buses emptier.

He might also have asked himself whether taxpayers weren’t already bearing more than their fair share of the burden. The channels through which subsidies flow from taxpayers’ pockets to IndyGo’s coffers are many and varied, and some involve rent-seeking activity that seems designed to obscure the subsidies’ source. IndyGo’s CEO recently claimed, for example, that “as per the Board of Accounts for the State of Indiana federal taxes and state taxes are not considered taxes . . . . They’re considered grants.” But most of the subsidy comes from local taxes, and bureaucratic doublespeak doesn’t change the fact that the sources of those “grants” are gasoline, sales, and other taxes, all of which reduce what taxpayers have left to pay for things like hearing-aid batteries, kids’ braces, and water-heater replacements.

Comparing the taxpayer burden with the fares paid by riders, the plot above shows that the people actually taking the bus rides weren’t contributing even one-fifth of IndyGo’s revenue. So legislators might have been forgiven for believing that riders, not taxpayers, were the ones who should bear any increased burden. Perhaps as a result the following compromise was struck:

IC 36-9-4-58(b) If a public transportation corporation providing public transportation services in Marion County expands its service through a public transportation project authorized and funded under IC 8-25, the public transportation corporation shall establish fares and charges that cover at least twenty-five percent (25%) of the operating expenses of the urban mass transportation system operated by the public transportation corporation.

In addition to its regular-bus system, which follows fixed routes, IndyGo operates a van system, whose vehicles instead go where riders direct them. But the operating expenses that the 25% threshold was to be based on were only those of the fixed-route system:

For purposes of this subsection, operating expenses include only those expenses incurred in the operation of fixed route services that are established or expanded as a result of a public transportation project authorized and funded under IC 8-25.

With that proviso, the statute enabled the Council to increase IndyGo’s burden on taxpayers only if IndyGo’s riders contributed significantly more than they had been.

Fig. 3 illustrates what would have been apparent when the transit-tax bill was being considered: that to obtain the transit tax IndyGo would have to increase ridership and/or fare price significantly. Fig. 3’s green curve represents what Federal Transit Administration (“FTA”) data say had been IndyGo’s recent fixed-route fare collections. The FTA data’s operating-expense values don’t include depreciation, but if we allocate to IndyGo’s fixed-route system the same percentage of IndyGo’s reported total operating expenses as the FTA data allocate to it out of non-depreciation operating expenses then the red curve represents the minimum fare revenue that would have met the statutory requirement.

Based on those values the fare-price increase that in the absence of a ridership reduction would have qualified IndyGo to impose a transit tax was, depending on the year, between 25% and 50%. If operating expenses increased—as they inevitably would if IndyGo used the transit tax to expand its operations—then the fare-price increase would need to be higher still unless ridership increased proportionately.

But transit-tax proponents have argued that the required farebox-recovery ratio could be satisfied without any significant fare-price increase; the transit-tax-funded bus-frequency increases and bus-hours extensions, they said, would unleash pent-up demand. So that was the deal: the tax could be imposed without significant fare-price increases if proponents turned out to be right, but if they turned out to be wrong IndyGo would have to raise fare prices or forgo the transit tax.

Voters approved that deal in response to a massive (and in many ways misleading) propaganda campaign. The Council thereupon imposed the tax in early 2017 in response to several IndyGo presentations urging it to do so.

IndyGo Never Expected to Comply

Calling those IndyGo presentations misleading would be an understatement. At their heart was a twenty-year financial plan whose fare-revenue projections have so far proved to be wildly optimistic; the $5.8 million that IndyGo collected last year, for example, was less than a third of the $19.4 million the plan projected:

To place the plan’s above-listed projections in context the left, historical portion of Fig. 4 below estimates what the fixed-route components of Fig. 2’s quantities probably were:

In reporting IndyGo’s fare revenue and operating expenses the FTA data provide separate bus- and van-service numbers, so for fare-revenue values Fig. 4’s left portion simply uses (inflation-adjusted versions of) the FTA’s numbers for the fixed-route service’s fare revenue. But IndyGo’s annual reports tend not to list values for its regular-bus system separately from those for its van system. So the left portion’s estimates of how much tax revenue went to IndyGo’s fixed-route services were calculated as the products of the local-, state-, and federal-tax-revenue numbers from IndyGo’s annual reports and the ratios that the FTA’s values for fixed-route-only operating expenses net of depreciation bear to the sums of those values and the corresponding van-system values.

Fig. 4’s right-hand portion represents the financial plan’s projections. It shows that the fares IndyGo projected don’t come close to covering 25% of the projected IndyGo burden. The values in that plot portion were calculated by backing out the 1.6%-per-year inflation assumption that IndyGo’s numbers were based on and allocating portions of the resultant quantities to the regular, fixed-route bus system. The transit tax was allocated entirely to the regular-bus system, while the other taxes were so allocated as to divide the plan’s fare-and-tax total between the bus and van systems in the proportions implied by the values the plan gave for total and van-system-only operating expenses.

Now, Fig. 5 shows that the accounting IndyGo used in its financial plan came up with operating-expense values significantly lower than the values it projected for revenues. Despite being based on these low values and IndyGo’s wildly optimistic fare-revenue projections, however, Fig. 6’s projected farebox-recovery ratios amount to less than 18%. So IndyGo never really intended to comply with the fare-recovery requirement.

Yet its financial plan stated that farebox recovery would reach 29% by 2022. As can be seen at 1:22:20 et seq. in a Council-meeting video, its rationale for claiming so high a percentage was that the statute’s 25% requirement shouldn’t be viewed as based on all of IndyGo’s fixed-route-services’ operating expenses:

The 25% farebox recovery that is covered in the statute? That is on the direct operating expenses of the expanded service. If you look at our overall budget today and the fare recovery as a proportion, we’re sitting at about nineteen, twenty percent currently, and that’s not the direct operating cost for the service, so if you look at just the direct operating cost today we’re about twenty-two, twenty-three percent. When we deploy frequent service and attract more ridership, we’ll easily hit that requirement.

Fig. 6 shows that in reality the farebox-recovery percentage had fallen to about 15% by the time IndyGo told the Council in early 2017 that “we’re sitting at about nineteen, twenty percent currently.” And, as comparison with IndyGo’s own annual reports will presently reveal, IndyGo couldn’t honestly have believed that the statute’s 25% requirement was intended to be based only on what IndyGo called “direct” operating expenses.

First, though, note that the way in which IndyGo came up with such inflated farebox-recovery values was to ignore nearly half of the projected operating expenses. Take the financial plan’s 29% farebox-recovery projection for last year. Out of the $123,802,419 in operating expenses projected by the financial plan for 2022, IndyGo apparently excluded from “direct” operating expenses everything but the $45,803,998 and $17,052,078 it listed as the “delivery costs” of “local route” and “BRT” services respectively. (Local route is IndyGo’s terminology for a non-BRT fixed route.) Among the operating-expense quantities excluded from those “delivery costs” were “Vehicle Maintenance Costs,” “BRT Infrastructure Maintenance Costs,” “Administrative Costs,” and “Paratransit Operating Costs.”

Now, paratransit is IndyGo’s term for its van service, so excluding “Paratransit Operating Costs” was appropriate. But “BRT Infrastructure Maintenance Costs” clearly apply to the fixed-route system alone, and the overwhelming majority of the “Vehicle Maintenance Costs” and “Administrative Costs” would be allocable to that system even if the van system’s share of maintenance and administrative costs weren’t already included in “Paratransit Operating Costs.” Yet IndyGo excluded them. (As can be seen at 1:32:20 et seq. in one of the Council-meeting videos, the Council’s Municipal Corporations Committee was warned about this creative accounting at the time, but it seemed to ignore that warning.)

By dividing the $112,877,495 IndyGo projected for operating expenses net of paratransit cost into the $18.2 million (29% of the sum of $45,803,998 and $17,052,078) it apparently projected as the fixed-route portion of that year’s fare revenue we see that if IndyGo hadn’t excluded those cost elements the fare-recovery percentage would have been only 16%. This still would have overstated fare recovery, because the financial plan omitted depreciation. And that percentage was based on a ridership projection that we warned the Council was too optimistic.

As we stated above, IndyGo couldn’t honestly have believed that the statute justified the unconventional farebox-recovery calculation the financial plan used. The term direct appears nowhere in the relevant statutory provision; the statute merely says “operating expenses.” And there’s no reason to believe that the General Assembly intended operating expenses to have any meaning other than the conventionally inclusive one accorded it by IndyGo’s annual reports, which encompasses “Transportation,” “Maintenance of equipment, including fuel,” “Administrative and general,” “Claims and Insurance,” and “Depreciation.” IndyGo’s strained construction of “operating expenses” seems to have been nothing more than an attempt to disguise its evasion of the statutory limitation.

Conclusion

We have argued elsewhere that IndyGo’s transit-tax-funded expansion has actually reduced Indianapolis mobility and is on track to reduce it further. Since neither IndyGo nor the Council can be counted on to abide by statutory limitations, the statute should be repealed before Indianapolis suffers any further damage. Or, if the statute isn’t completely repealed, it should at least be revised as the next post will suggest to make flouting the statutory requirements more difficult.

Government is and has always been a criminal enterprise. Indygo will build more infrastructure that can't/won't be maintained and spend the next 50 years (until it is demolished and rebuilt as some other boondoggle) begging for more funding to maintain it, indicating that the lack of ridership is due to low funding instead of low interest. The people that support this type of stuff are people who want to brag to their fellow government sycophants what cool stuff they have (they really want light rail) but they have convinced themselves that BRT is actually something meaningful (it is not).

“Nearly half a century ago [IndyGo] began resorting to government subsidies instead of right-sizing its operations as erstwhile bus riders became increasingly able to afford cars.”

That’s not what happened. In 1973 Congress passed the Federal-Aid Highway Act reauthorizing funding the interstate highway system. But this time a contentious debate led to an amendment that directed spending to bus systems and other forms of public transit.

So what happened is not that the government decided to prop up a failing business. Rather, the duly elected representatives of the people agreed that public subsidy of transportation should include both highways *and* funding for programs like bus systems.