Revise Indiana's Transit-Tax Statute

Its Requirements Aren't Being Enforced

Introduction

The previous post observed that Indiana’s transit-tax statute appears to have been based on a false assumption. According to that statute the fixed-route system of the Indianapolis Public Transportation Corporation (“IndyGo”) must collect at least 25% of its operating expenses as fare revenue if the Indianapolis City-County Council imposes a transit income tax in its favor. The Indiana General Assembly seemed to assume that the Council and/or IndyGo would enforce that requirement. Instead, they’ve flouted it for six years, imposing the tax without collecting the required fare revenue. So the previous post argued that the General Assembly should repeal the statute.

Failing that, the General Assembly should so revise the statute as to make the fare requirement harder to evade, and this post will propose such revisions. One of the proposed revisions is that the statute require the Indiana Department of Revenue to deny any Council request for transit-tax collection unless the farebox-recovery requirement is met. Another is that the test for compliance be made more certain by basing it on collected rather than expected revenue. Specifically, tax collection in an upcoming calendar year should be denied if IndyGo failed to satisfy the fare requirement in the most-recent calendar year for which farebox-recovery data are available.

A further revision could be to base the fare-revenue criterion on a quantity that is less susceptible to manipulation than operating expense can be. Specifically, the criterion for permitting transit-tax collection could instead be that the base year’s fare revenue be at least 0.19% of that year’s income-tax base, i.e. of the quantity that results from dividing that year’s income-tax receipts by its income-tax rate.

Background

Before we discuss the proposed revisions in more detail we’ll extend the previous post’s discussion of why repealing the statute outright would be better. As that post said, IndyGo’s real problem is that it’s just too big for the city’s bus-ride market. A consequence of that problem is that the cost of providing a bus ride has become exorbitant. Taxpayers are not just paying much more for other people’s bus rides than they pay for their own transportation. They’re paying more for those rides than the rides are worth to the riders themselves.

Consider what we ordinarily pay for transportation. A $118 plane ticket to New York amounts to about 25¢ per passenger-mile. Even to a resident who buys a brand-new car every five years instead of holding it for the twelve-year average a modest-priced car would cost about 40¢ per passenger-mile. (If the urban-average car occupancy is 1.25 passengers per car, then the $38,723 given by Edmunds as the five-year true cost to own a Toyota Corolla driven 15,000 miles a year translates to 41¢ per passenger-mile.)

We saw in the previous post that IndyGo operates a paratransit, “demand-response” van system for the disabled in addition to its regular, “fixed-route” bus system. FTA data tell us how many passenger-miles IndyGo’s fixed-route system has provided, and the values plotted in Fig. 1 were obtained by dividing that quantity into the result of allocating portions of reported tax-receipt values to that system in the manner described by the previous post. Those results show that since the transit-tax bill was passed IndyGo’s fixed-route transportation cost has grown from around four to as much as sixteen times the cost of car transportation.

Indeed, IndyGo transportation has even come to cost more than taking a taxi. If we (somewhat arbitrarily, to be sure) assume that 70%, 22%, 6%, and 2% of cab rides are respectively taken by one, two, three, and four passengers per cab, then the average cost including a 20% tip of traveling the IndyGo-trip-average 4.4 miles by cab would be $2.35 per passenger-mile. So even before the pandemic the transit-tax-funded expansion had made IndyGo trips more costly than cab rides. And last year the cost of providing a single IndyGo bus ride was almost three times what traveling the same distance by cab would cost.

Of course, that ratio will decrease somewhat as federal funding falls from its temporary peak and ridership recovers a little more. But unless IndyGo is right-sized IndyGo transportation will probably never again fall below the cost of a cab—which is more than five times what cars cost.

Residents aren’t very often willing to pay that much for their own transportation. The average person travels something like 14,000 miles per year by car. The cost of doing that much traveling by cab would exceed Marion County’s $31,668 per capita income; there would be no money left for food, clothing, or shelter. In short, the cost of providing IndyGo bus rides is exorbitant.

For riders, though, rides are getting cheaper. IndyGo has surreptitiously reduced the average fare price, presumably through giveaways and transit-pass pricing.

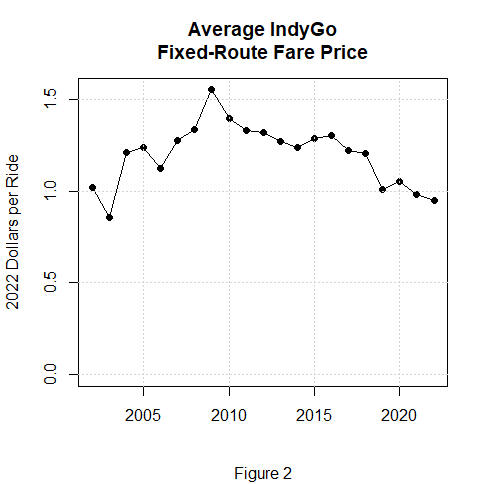

Dividing FTA data for the numbers of IndyGo fixed-route bus rides into the corresponding fare-revenue numbers yields Fig. 2’s values of average fare price. They show that despite the nominal full-fare price of $1.75 the average price has fallen over the past decade to less than a dollar. That is, falling ridership is not the only thing that has been increasing taxpayers’ share of the burden. IndyGo has actively thwarted the statutory goal of allocating the burden more equitably.

So the transit tax should be repealed. Failing that, the General Assembly should so revise the statute as to carry out the statutory goal more effectively. We now turn to revisions that could serve that purpose.

Two Revisions

Again, two of our proposals are (1) that the fare requirement be based on actual past revenue instead of on estimates of future revenue and (2) that the Department of Revenue refuse any request to collect transit tax unless the fare requirement has been met.

These revisions would require the Council to demonstrate to the Department’s satisfaction that in the last year for which a comprehensive financial statement is available IndyGo had satisfied the fare-recovery requirement.

In the case of 2024, for example, the 2022 statement would be the most-recent one. As can be seen above, that statement lists $5,667,742 in “Passenger fares” and $127,295,295 in “Total operating expenses.” In 2022, that is, fares covered only 4% of expenses, so under our proposal the transit tax couldn’t be imposed in 2024.

Since IndyGo’s statements don’t typically segregate its bus system’s expenses from its van system’s, the values listed above encompass more than just the portion of IndyGo’s operations to which the statute currently restricts the fare requirement. But basing the standard on those totals may be better than relying on IndyGo to divide operating expenses fairly between its bus and van systems: making totals the basis would leave less room for creative accounting.

Now, it’s true that basing a given percentage requirement on both systems together instead of on the fixed-route system alone would ordinarily require fixed-route fare revenue to be slightly greater. But if we apply that approach to the IndyGo projections described in the previous post we find the required fixed-route fare revenue would still average less than 26% of the fixed-route system’s operating expenses. A difference that small wouldn’t be nearly enough to compensate for riders’ having evaded their statutory share of the burden for the past six years.

Alternative Revisions

The foregoing proposal has the virtue of simplicity; to determine whether the fare-recovery requirement has been met the Department of Revenue needs only to divide one line item in IndyGo’s annual report by another. Since it’s based on operating expenses, though, it may be subject to manipulation. Less subject to manipulation would be the Marion County personal income-tax base: the result of dividing the base year’s income-tax receipts by that year’s tax rate. An alternative proposal would therefore be that the transit income tax not be imposed unless fare collections have equaled at least a certain percentage of that tax base. The percentage we propose below is 0.19%.

To understand the rationale behind this alternative let’s first note that the existing requirement—i.e., the requirement that fares cover 25% of operating expenses—may seem to imply that taxpayers bear no more than 75% of the burden. In other words, it may seem to imply that taxpayers won’t pay more than three times as much as riders do.

Indeed, that could have been what many General Assembly members had in mind when they voted for the transit-tax bill. Depreciation, after all, is one of the items that IndyGo’s annual statements routinely include in their values for operating expenses, so as capital assets are depreciated the revenues that had been expended on them and therefore omitted initially from operating expenses should tend over time to be recaptured. And as a public corporation IndyGo makes no payments to shareholders, so over time expenditures should roughly equal revenues.

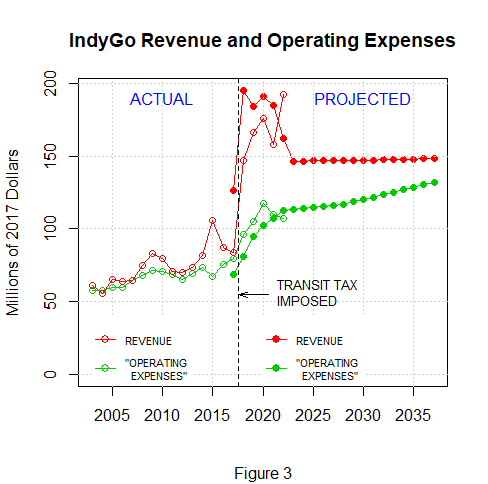

Furthermore, by comparing operating expenses with revenues net of bond proceeds Fig. 3 shows that this view may have seemed reasonable when the General Assembly passed the transit-tax bill in 2014. But we saw in the previous post that when IndyGo was lobbying for the transit tax it was selective about which of its financial plan’s operating-expense elements it included in its farebox-recovery calculation. And Fig. 3’s right-hand portion shows that even if we include all of the omitted elements the result falls short of what IndyGo really costs.

Now, that discrepancy results to a great degree from the fact that as a cash-flow study IndyGo’s financial plan didn’t include values for depreciation, whereas we saw that IndyGo’s annual financial statements do. So if the farebox-recovery criterion is based on operating expenses as presented in IndyGo’s annual comprehensive financial reports we would expect less of a discrepancy. Still, that discrepancy illustrates how the meaning of operating expenses can be manipulated. And even in the annual reports it’s not clear that the operating-expense numbers capture all element of the burden.

So basing the threshold on the income-tax base may have advantages, and Fig. 4 compares that alternative with other approaches. The red curve represents 25% of the projected sum of taxes and fares: the fare revenue that under IndyGo’s projections would limit the taxpayer share of the burden to no more than 75%. Again, IndyGo didn’t project depreciation values, so none of the Fig. 4 quantities includes it as a component. But the blue curve represents 25% of all operating costs that IndyGo’s financial plan did project. Comparing the blue curve with the red one reveals that it doesn’t even come close to 25% of the burden that taxpayers and riders would share.

Now, a reasonable approximation of the red curve’s 25% of the total burden would be one-third of the sum of the “Nonoperating Revenue” and “Capital Contributions” entries in the IndyGo annual report’s above-copied “Changes in Net Position” table. As the left portion of Fig. 4’s red curve illustrates, though, such a quantity can be volatile, so using it as the threshold could make it hard to predict what fare-revenue level will be adequate.

On the assumption that the income-tax base will be less volatile we therefore propose instead the fare-revenue threshold represented by the green curve: 0.19% of that tax base. (The fact that the green curve’s slope is steeper than the red curve’s is largely an artifact of the financial plan’s assumption that not all tax proceeds would grow in proportion to the population increase that the financial plan assumes will raise the income-tax base.)

Again, basing the threshold on the tax base has the advantage that it leaves little room for interpretation. That advantage would have to be weighed against the fact that our selection of the particular percentage was based on IndyGo projections of other taxes, and those will inevitably be somewhat inaccurate.

This Was the Deal

As Fig. 4’s dashed line indicates, even the optimistic fare-revenue projection that IndyGo used to convince the Council to impose the transit tax falls far short of all three illustrated thresholds. As a consequence, IndyGo and its supporters would probably object that such thresholds effectively prevent imposition of the transit tax. But 25% of operating expense was the deal they made with the General Assembly and that residents voted on.

It was IndyGo personnel who said the 25% threshold could easily be met with little or no fare-price increase. If that was a misrepresentation, then IndyGo should accept the consequences.

This is particularly true in light of the fact that voters have received very little of what they were promised in return for the tax. Note in this connection that IndyGo presentations such as the one that included the chart above claimed that by last year IndyGo would have 70% more buses on the streets and would whisk passengers rapidly along the dedicated lanes of three so-called bus-rapid-transit (“BRT”) lines. But although the transit tax has been collected for nearly six years now the average number of buses on the streets according to the Federal Transit Administration (“FTA”) was only 12% higher last year than it had been in 2016—and IndyGo has managed to put into operation only a single one of those three BRT lines that were supposed to have been completed by now.

Not only that, but the sole BRT line that IndyGo has managed to complete has seriously underperformed. Its ridership is less than a third of what IndyGo “conservatively” projected. The articulated buses used on that line are more accident-prone than IndyGo’s other buses. According to the ratio of revenue-mile to revenue-hour values in the FTA’s data the BRT-line buses’ speeds exceed other buses’ by less than 4% despite the dedicated lanes; this minuscule speed difference probably saves riders less time in riding the bus than the BRT line’s greater stop spacing costs them in walking to and from bus stops. After four years of operation, moreover, the BRT line’s special off-board fare-collection equipment still doesn’t function reliably, and its drivers haven’t mastered either staying in their dedicated lanes or bringing buses close enough to their platforms for wheelchair access.

In short, IndyGo has delivered very little of what it promised it would in return for the transit tax. So discontinuing the tax at least until the necessary ridership materializes would be only proper.

Conclusion

Most of the assumptions the transit-tax statute was based on have turned out to be false. In particular, fare revenue hasn’t come even close to the statutory 25% threshold, yet IndyGo has continued to collect the transit tax. As a consequence, the cost of IndyGo transportation has become exorbitant; the burden that IndyGo imposes on taxpayers far exceeds the value of the bus rides it provides to riders. If the General Assembly doesn’t put a stop to this obscene waste of taxpayers’ money it should at least ensure that the intended limitations are enforced.

“IndyGo’s real problem is that it’s just too big for the city’s bus-ride market.”

Transit authorities are not businesses attempting to meet a market need at a price which can sustain operations. They are public services. They are expected to operate at a loss.

This is not unique to Indianapolis. Most systems barely recover much of their cost at farebox:

https://www.transitwiki.org/TransitWiki/index.php/Farebox_Recovery_Ratio

Granted, there is a discussion to be had about the value of services that do not pay for themselves. Elementary schools don’t manage to make enough in textbook fees to pay teachers. Nor do building permits cover administrative costs or fines pay for police departments. But the issue of farebox recovery is common everywhere.

Certainly the legal issues you raise are valid and are a disappointing reminder.